Lesson 9: Yield Optimization Strategies

🎯 Core Concept: Maximizing Returns While Managing Risk

Yield optimization in money markets requires balancing multiple factors: supply rates, borrow costs, leverage, gas fees, and risk. This lesson teaches you to calculate true yields, execute looping strategies safely, and identify cross-protocol arbitrage opportunities.

📊 Supply Rate Maximization

Understanding True Yield

Components of Yield:

- Base supply APY

- Protocol rewards (if applicable)

- Compounding frequency

- Gas costs (relative to position size)

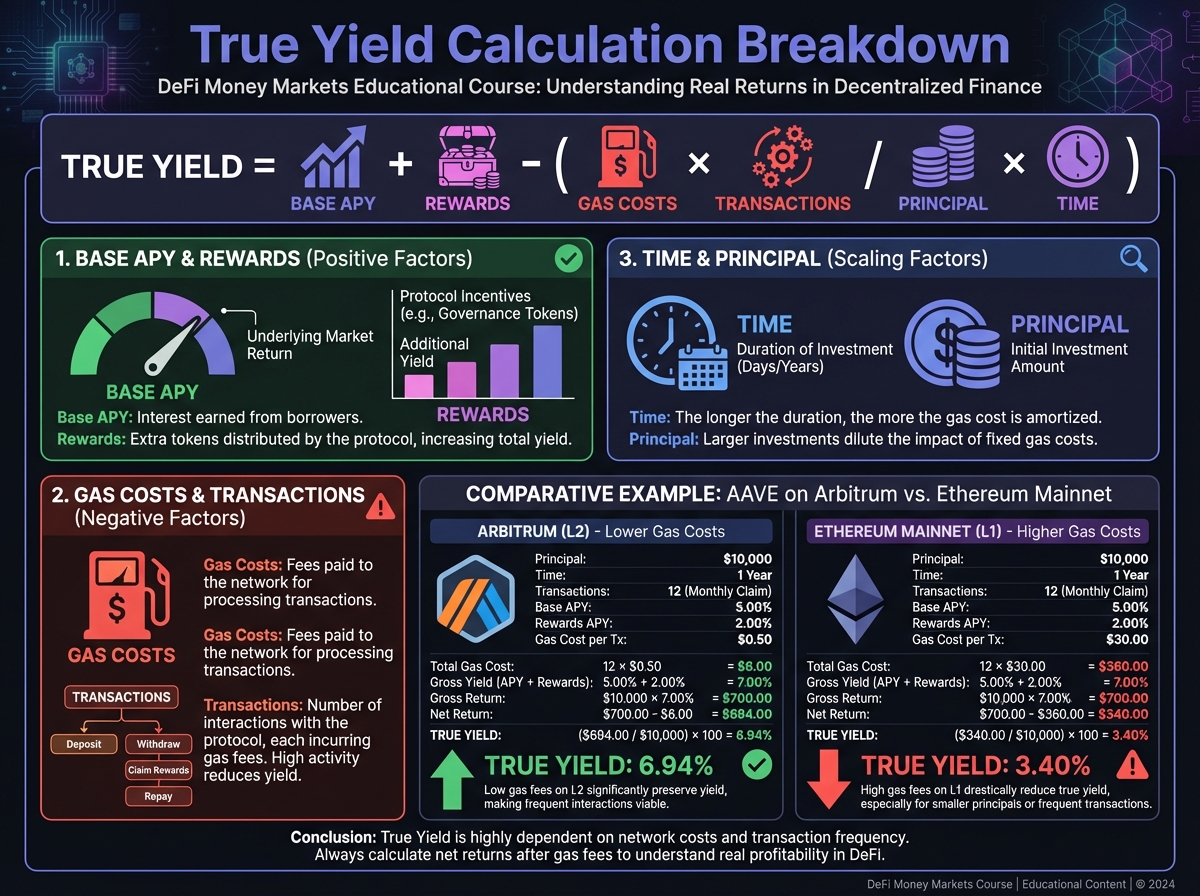

True Yield Formula: $$True Yield = Base APY + Rewards - \frac{Gas Costs \times Transactions}{Principal \times Time}$$

Example:

- Base APY: 5%

- Gas per transaction: $0.50 (on L2)

- Transactions per year: 12 (monthly compounding)

- Principal: $10,000

- True yield: 5% - ($0.50 × 12) / $10,000 = 4.94%

Supply Rate Factors

1. Utilization Rate

- Higher utilization = higher supply rates

- Monitor utilization trends

- Move funds to higher-utilization pools when appropriate

2. Network Selection

- L2s (Arbitrum/Base): Lower gas, lower yields

- Mainnet: Higher gas, potentially higher yields

- Calculate break-even point based on position size

3. Stablecoin vs Crypto

- Stablecoins: Lower yields, lower risk

- Crypto: Higher yields (if used as collateral), higher risk

- Balance based on risk tolerance

💰 Borrow Rate Optimization

When Borrowing Makes Sense

1. Leverage Strategies

- Amplify yields on yield-bearing assets

- Example: Stake ETH (5% APY), borrow against it (4% cost) = 1% net + leverage

2. Arbitrage Opportunities

- Borrow low, lend high (different protocols)

- Example: Borrow USDC at 4% on Aave, lend at 6% on Morpho = 2% spread

3. Tax Efficiency

- Borrow against assets instead of selling

- Avoid taxable events

- Interest may be tax-deductible (consult tax professional)

Calculating Borrow Profitability

Net Yield Formula: $$Net Yield = (Asset Yield \times Leverage) - (Borrow Rate \times (Leverage - 1))$$

Example:

- Asset yield: 7% (JitoSOL staking)

- Leverage: 3x

- Borrow rate: 5%

- Net yield: (7% × 3) - (5% × 2) = 11% APY

Break-Even Point: $$Break-Even = \frac{Borrow Rate \times (Leverage - 1)}{Leverage}$$

If borrow rate exceeds this, position becomes unprofitable.

🔄 Looping Strategies

What is Looping?

Definition: Borrowing against collateral to buy more of the same asset, repeating the process to amplify exposure.

Steps:

- Deposit asset as collateral

- Borrow stablecoins

- Buy more of the asset

- Deposit as collateral

- Repeat

Manual Looping (Step-by-Step)

Example: Loop ETH position

Initial: 10 ETH @ $2,000 = $20,000

Iteration 1:

- Deposit 10 ETH (LTV 75%, max borrow $15,000)

- Borrow $10,000 USDC (conservative 50% of max)

- Buy 5 ETH with $10,000

- Total: 15 ETH collateral, $10,000 debt

Iteration 2:

- Deposit 5 new ETH (total 15 ETH)

- Borrow $5,000 USDC

- Buy 2.5 ETH

- Total: 17.5 ETH collateral, $15,000 debt

Result: 17.5 ETH exposure from initial 10 ETH (~1.75x leverage)

Automated Looping (Kamino Multiply)

Advantage: Atomic transactions—all steps in one block

How It Works:

- Protocol handles all steps automatically

- Flash loans eliminate intermediate capital needs

- Single transaction = lower gas + lower slippage risk

Example: JitoSOL Multiply

- Deposit 10 JitoSOL

- Set 3x leverage

- Protocol automatically loops

- Receive 3x exposure in single transaction

Loop Risk Management

Critical Rules:

- Monitor Health Factor: Keep HF > 2.0 minimum

- Calculate Break-Even: Know when position becomes unprofitable

- Set Stop-Loss: Define exit strategy before entering

- Start Small: Test with small positions first

- Understand Liquidation: Know exact liquidation price

Liquidation Price Formula: $$Liquidation Price = \frac{Debt}{Collateral \times LT}$$

Monitor constantly—loops amplify liquidation risk.

🌐 Cross-Protocol Arbitrage

Identifying Opportunities

Opportunities Arise When:

- Utilization differences across protocols

- Interest rate spreads

- Reward programs

- Temporary market inefficiencies

Example Scenario:

- Aave USDC supply: 4% APY

- Morpho USDC vault: 5.5% APY

- Spread: 1.5% APY

Strategy: Move funds from Aave to Morpho to capture spread.

Execution Considerations

1. Gas Costs

- Calculate if spread covers gas

- L2s reduce gas burden

- Minimum viable position size

2. Withdrawal Limits

- Check if immediate withdrawal possible

- Monitor idle liquidity on target protocol

- Have backup plan if withdrawal delayed

3. Risk Differences

- Understand protocol risk profiles

- Assess if extra yield compensates extra risk

- Consider insurance coverage differences

📈 Advanced Optimization Techniques

Compound Frequency Optimization

Understanding Compounding:

- More frequent compounding = higher effective yield

- But requires more transactions = more gas

Optimal Frequency:

- Small positions: Quarterly or annually

- Large positions ($50k+): Monthly or weekly

- Very large positions: Daily (if gas justified)

Formula: $$Effective APY = (1 + \frac{APY}{n})^n - 1$$

Where n = compounding frequency per year.

Multi-Protocol Diversification

Strategy: Split capital across multiple protocols

Benefits:

- Diversify protocol risk

- Capture best rates per protocol

- Avoid single point of failure

Example Allocation:

- 40% Aave (safety, insurance)

- 30% Morpho (efficiency)

- 20% Euler (customization)

- 10% Kamino (leverage strategies)

Yield Aggregators

What They Are: Protocols that automatically optimize across money markets

Examples: Yearn, Beefy, Convex

Pros:

- Automated optimization

- Gas-efficient rebalancing

- Professional management

Cons:

- Additional smart contract risk

- Fees (performance + management)

- Less control over strategy

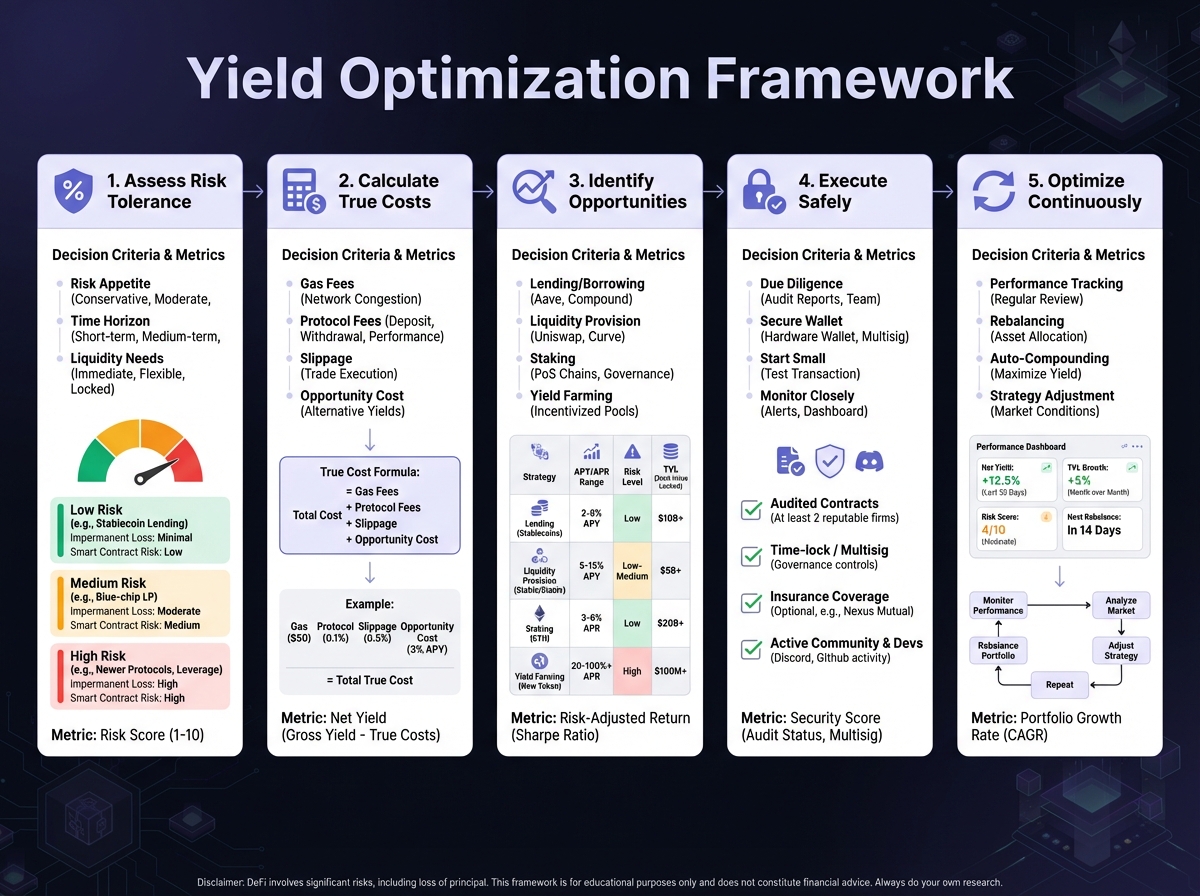

🎯 Yield Optimization Framework

Step 1: Assess Risk Tolerance

- Conservative: Supply stablecoins only, HF > 2.0

- Moderate: Some leverage (1.5-2x), blue-chip collateral

- Aggressive: Higher leverage, diversified protocols

Step 2: Calculate True Costs

- Base yields

- Gas costs

- Protocol fees

- Opportunity costs

Step 3: Identify Opportunities

- Monitor rate differences

- Track utilization changes

- Watch for reward programs

- Assess cross-protocol spreads

Step 4: Execute Safely

- Start small to test

- Monitor positions closely

- Have exit strategy

- Keep reserves for emergencies

Step 5: Optimize Continuously

- Review positions weekly

- Rebalance when spreads change

- Adjust for risk tolerance changes

- Track performance vs benchmarks

⚠️ Common Optimization Mistakes

Mistake 1: Chasing highest yield without considering risk

- Fix: Always assess risk-adjusted returns

Mistake 2: Ignoring gas costs

- Fix: Calculate true yield after fees

Mistake 3: Over-leveraging

- Fix: Keep HF > 2.0, understand liquidation risk

Mistake 4: Not monitoring positions

- Fix: Set up alerts, check daily

Mistake 5: Ignoring protocol differences

- Fix: Understand risk profiles, don't assume all protocols equal

📊 Real-World Optimization Example

Scenario: $50,000 to optimize

Option A: Aave only

- Supply USDC: 5% APY

- Annual earnings: $2,500

Option B: Diversified

- $20k Aave: 5% = $1,000

- $20k Morpho: 5.5% = $1,100

- $10k Kamino (2x leverage JitoSOL): 11% net = $1,100

- Total: $3,200

- Extra yield: $700 (28% improvement)

Risk: Higher (leverage + protocol diversification)

🔧 Interactive Tools

Interactive Looping Calculator

Calculate leverage, net yield, and break-even rates for looping strategies:

Launch Interest Accrual Simulator →

🔑 Key Takeaways

- True yield = Base APY + rewards - gas costs

- Looping amplifies returns but increases liquidation risk

- Cross-protocol arbitrage captures rate spreads

- Calculate break-even for all strategies

- Monitor constantly—rates and risks change

- Start conservative—optimize incrementally

🚀 Next Steps

Lesson 10 explores advanced risk management and hedging strategies—protecting positions during volatility, managing multi-protocol portfolios, and building comprehensive risk frameworks.

Complete Exercise 9 to build your yield optimization framework.

Remember: Optimization is about maximizing risk-adjusted returns, not just raw yield. Balance efficiency with safety.

← Back to Summary | Next: Exercise 9 → | Previous: Lesson 8 ←