Lesson 8: Risk Management and Hedging Strategies

🎯 Core Concept: Protect Capital First

Professional LPs don't just earn fees—they manage risk. This lesson teaches advanced risk management techniques including delta hedging, LVR mitigation, and portfolio-level risk controls.

🛡️ The Risk Management Framework

Three Types of Risk

1. Impermanent Loss (IL):

- Opportunity cost vs. holding

- Reversible if price returns

- Mitigated by: Stable pairs, hedging

2. Loss Versus Rebalancing (LVR):

- Value extracted by arbitrageurs

- Never reversible (monotonic)

- Mitigated by: Lower volatility pairs, faster chains

3. Smart Contract Risk:

- Bugs, exploits, hacks

- Permanent loss

- Mitigated by: Audited protocols, diversification

📊 Delta Hedging Strategy

The Concept

Delta = Sensitivity of position to price changes

Delta Hedging = Neutralize price exposure, profit only from fees

How It Works

Step 1: Provide liquidity (long both assets)

- Example: 1 ETH + 2,000 USDC in pool

- Delta: Long ETH exposure

Step 2: Short ETH to hedge

- Borrow ETH on Aave

- Sell ETH for USDC

- Delta: Short ETH exposure

Step 3: Net position

- Long ETH (from LP) + Short ETH (from borrow) = Delta neutral

- Profit: Fees - Borrowing costs

Complete Example

Setup:

- LP Position: $10,000 (5 ETH + 10,000 USDC at $2,000/ETH)

- Borrow: 5 ETH on Aave (50% LTV)

- Sell: 5 ETH for 10,000 USDC

- Net: Delta neutral

Monthly:

- LP Fees: $100

- Borrowing cost: $50 (5% APY on ETH)

- Net: $50/month (0.5% monthly = 6% APY)

If ETH drops 20%:

- LP IL: -$1,000

- Short profit: +$1,000

- Net: $0 (hedged!)

If ETH rises 20%:

- LP IL: -$1,000

- Short loss: -$1,000

- Net: $0 (hedged!)

Result: Isolated fee yield, no price exposure!

When to Hedge

Hedge if:

- ✅ Large positions ($50k+)

- ✅ Volatile pairs

- ✅ Want pure fee yield

- ✅ Can afford borrowing costs

Don't hedge if:

- ❌ Small positions (costs too high)

- ❌ Stable pairs (IL minimal)

- ❌ Want price exposure

- ❌ Can't afford borrowing

🔄 Portfolio Risk Management

Position Sizing

Rule 1: Never risk more than 5-10% per position Rule 2: Diversify across pairs, protocols, chains Rule 3: Correlated pairs count as one position

Correlation Matrix

High Correlation (count as 1 position):

- ETH/BTC

- wstETH/ETH

- USDC/USDT

Low Correlation (separate positions):

- ETH/meme coin

- Stablecoin/volatile asset

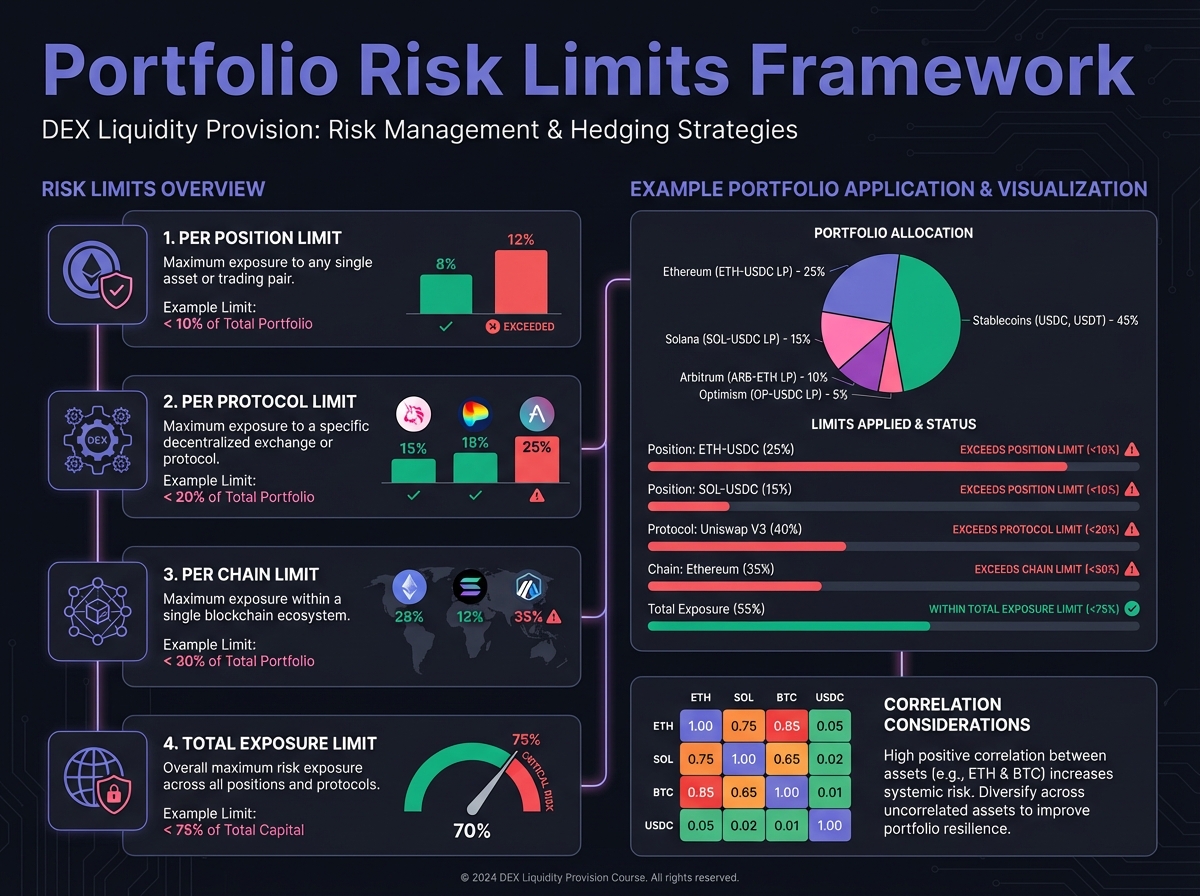

Risk Limits

Maximum Exposure:

- Single pair: 10% of portfolio

- Single protocol: 25% of portfolio

- Single chain: 50% of portfolio

Example ($100k portfolio):

- Uniswap V3 ETH/USDC: $10k (10%)

- Aerodrome WETH/USDC: $10k (10%)

- Raydium SOL/USDC: $10k (10%)

- Reserve: $70k (70%)

🎯 LVR Mitigation Strategies

Strategy 1: Lower Volatility Pairs

LVR Formula: LVR ∝ σ² (volatility squared)

Implication: Halving volatility = 4x less LVR

Action: Choose stable or correlated pairs

Strategy 2: Faster Chains

LVR is block-time sensitive:

- Ethereum (12s blocks): Higher LVR

- Arbitrum (0.25s blocks): Lower LVR

- Solana (0.4s blocks): Lower LVR

Action: Use L2s or alternative chains

Strategy 3: Dynamic Fees

Meteora adjusts fees with volatility:

- Higher volatility = Higher fees

- Compensates for increased LVR

Action: Consider Meteora for volatile pairs

🔬 Advanced Deep-Dive: Options-Based Hedging

Protective Puts

Strategy: Buy put options to protect downside

Example:

- LP Position: $10,000 ETH/USDC

- Buy: $10,000 put option (strike $1,800)

- Cost: $200 (2%)

If ETH drops to $1,600:

- LP Loss: -$1,000

- Put Profit: +$1,000

- Net: -$200 (just option cost)

If ETH stays above $1,800:

- LP: Normal returns

- Put: Expires worthless

- Net: -$200 (option cost)

Covered Calls

Strategy: Sell call options to generate income

Example:

- LP Position: $10,000 ETH/USDC

- Sell: $10,000 call option (strike $2,200)

- Premium: $150 (1.5%)

If ETH stays below $2,200:

- LP: Normal returns

- Call: Expires worthless

- Net: +$150 (premium earned)

If ETH rises above $2,200:

- LP: Normal returns (capped)

- Call: Exercised (sell ETH at $2,200)

- Net: Premium + capped gains

📈 Risk Monitoring Dashboard

Key Metrics to Track

Daily:

- Current IL vs. fees earned

- Position value changes

- Price vs. range boundaries

Weekly:

- Net PnL (fees - IL - gas)

- Comparison to holding

- Risk limit compliance

Monthly:

- Total return analysis

- Portfolio rebalancing

- Strategy adjustments

Risk Alerts

Set Alerts For:

- IL exceeds fees (losing money)

- Price exits range (V3)

- Position exceeds risk limits

- Gas costs exceed fees

🎓 Beginner's Corner: Risk Management Basics

Q: Do I need to hedge? A: Only for large positions ($50k+) or very volatile pairs. Start without hedging, learn first.

Q: How much should I risk? A: Start with 1-5% of portfolio per position. Increase as you learn.

Q: What if IL exceeds fees? A: Withdraw and reassess. Don't wait hoping it improves.

Q: Should I diversify? A: Yes! Across pairs, protocols, and chains. Don't put all eggs in one basket.

Q: How do I monitor risk? A: Use analytics tools (APY.vision, Revert Finance) or track manually weekly.

Interactive Rebalancing Strategy Planner

Use this tool to plan your rebalancing strategies and optimize risk management across your LP positions:

Launch Rebalancing Strategy Planner →

🔑 Key Takeaways

- Risk management protects capital - fees alone aren't enough

- Delta hedging isolates fee yield from price exposure

- Portfolio limits prevent catastrophic losses

- LVR mitigation requires low volatility or fast chains

- Options hedging is advanced but powerful

- Monitor risk metrics weekly to catch problems early

- Start conservative - increase risk as you learn

🚀 Next Steps

Module 3 covers elite operations: Uniswap V4, MEV tactics, governance, and building complete LP systems. These advanced topics require solid risk management foundations.

Complete Exercise 8 to develop your risk management framework and calculate hedging strategies.

Remember: Professional LPs manage risk first, optimize returns second. Protect your capital, and the fees will follow. Unmanaged risk destroys more LP positions than low fees.

← Back to Summary | Next: Exercise 8 → | Previous: Lesson 7 ←