Lesson 3: Architecture Types and Market Structure

🎯 Core Concept: Architecture Determines Everything

Understanding the architecture of a perpetual DEX is the single most critical factor in assessing risk and choosing the right platform for your strategy. The architecture dictates:

- How prices are discovered

- Where liquidity comes from

- What risks you face

- What fees you pay

- How fast trades execute

This lesson is foundational—master it before moving to protocol-specific lessons.

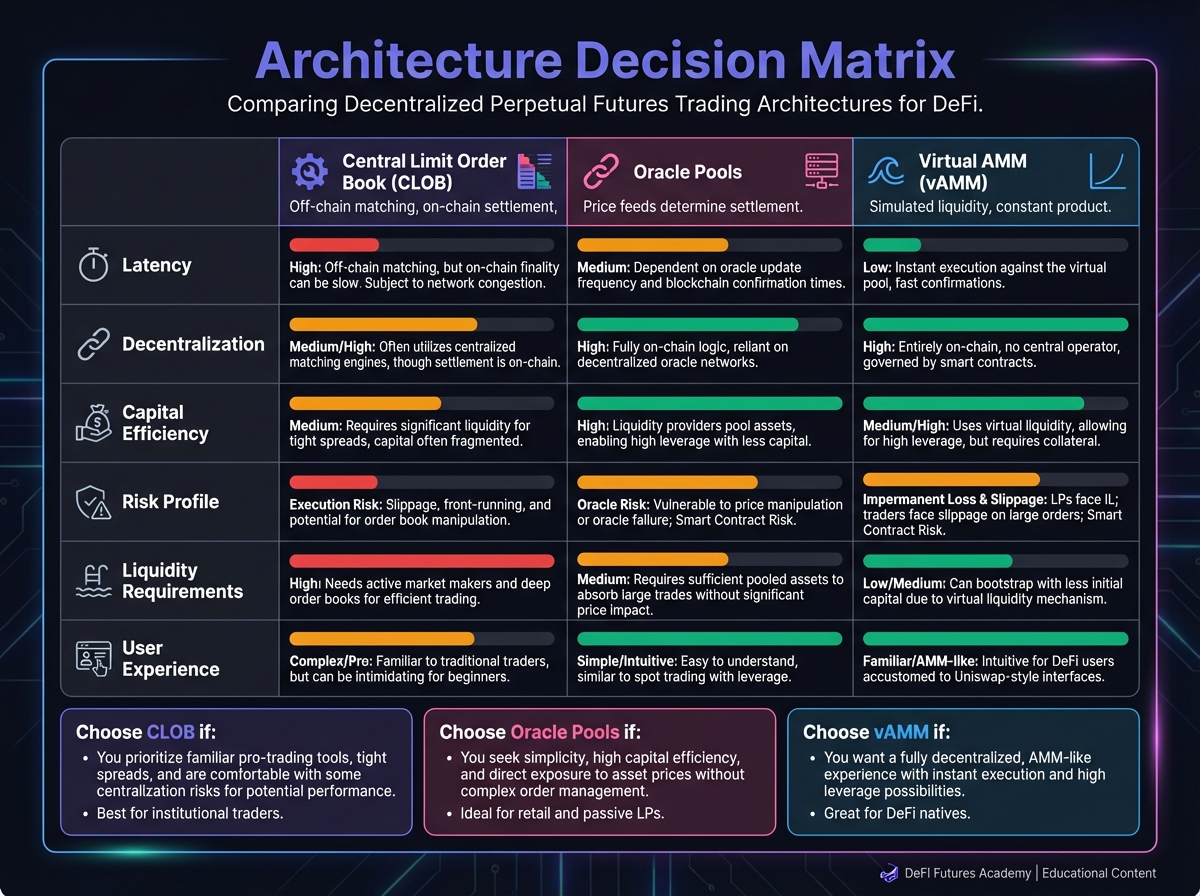

🏗️ The Three Architectural Models

The perpetual DEX market has evolved into three primary architectural categories:

- Central Limit Order Book (CLOB)

- Oracle-Based Shared Liquidity Pools

- Virtual AMM (vAMM)

Each model presents unique trade-offs regarding latency, decentralization, capital efficiency, and risk.

📚 Model 1: Central Limit Order Book (CLOB)

How CLOB Works

The CLOB model replicates the traditional exchange experience:

- Market Makers post buy/sell orders at specific prices

- Traders execute against the order book

- Price Discovery happens through supply and demand

- Matching occurs when buy and sell orders cross

Think of it like: A traditional stock exchange (NASDAQ, NYSE) but on-chain.

CLOB Sub-Models

Application-Specific Blockchains (AppChains)

Examples: dYdX v4, Hyperliquid

How It Works:

- Exchange runs on its own dedicated blockchain

- Optimized exclusively for trading activity

- High throughput and low latency

dYdX v4 (Cosmos SDK):

- In-memory order book maintained by validators off-chain

- Trades committed on-chain for settlement

- ~2,000 TPS capacity

- Decentralized matching engine (validators)

Hyperliquid (HyperEVM):

- Entire order book fully on-chain

- Custom consensus (HyperBFT) for low latency

- ~200,000 orders/second capacity

- Sub-second latency (0.2s)

Benefits:

- ✅ CEX-like performance

- ✅ Transparent order book

- ✅ Limit orders, stop losses

- ✅ Deep liquidity (if market makers active)

Risks:

- ❌ Slippage on large orders

- ❌ Front-running risk

- ❌ Requires active market makers

- ❌ Bridge risk (moving assets to AppChain)

Hybrid Off-Chain Matching

Examples: Vertex (Arbitrum), ApeX (StarkEx), EdgeX (Starknet)

How It Works:

- Off-chain sequencer matches orders (lightning fast)

- Trades settled on-chain (L2 rollup)

- Best of both worlds: CeFi speed + DeFi security

Benefits:

- ✅ Very low latency (<10ms matching)

- ✅ On-chain settlement (self-custody)

- ✅ No MEV (sequencer handles matching)

- ✅ Works on existing L2s

Risks:

- ❌ Sequencer centralization

- ❌ Trust in sequencer not to front-run

- ❌ Still requires bridging to L2

CLOB Characteristics

| Feature | Description |

|---|---|

| Price Discovery | Internal (supply/demand in order book) |

| Slippage | Yes (depends on order book depth) |

| Liquidity Source | Market makers providing quotes |

| Latency Risk | Front-running order placement |

| Trader Experience | CEX-like, limit orders, advanced order types |

| Capital Efficiency | High (market makers provide liquidity) |

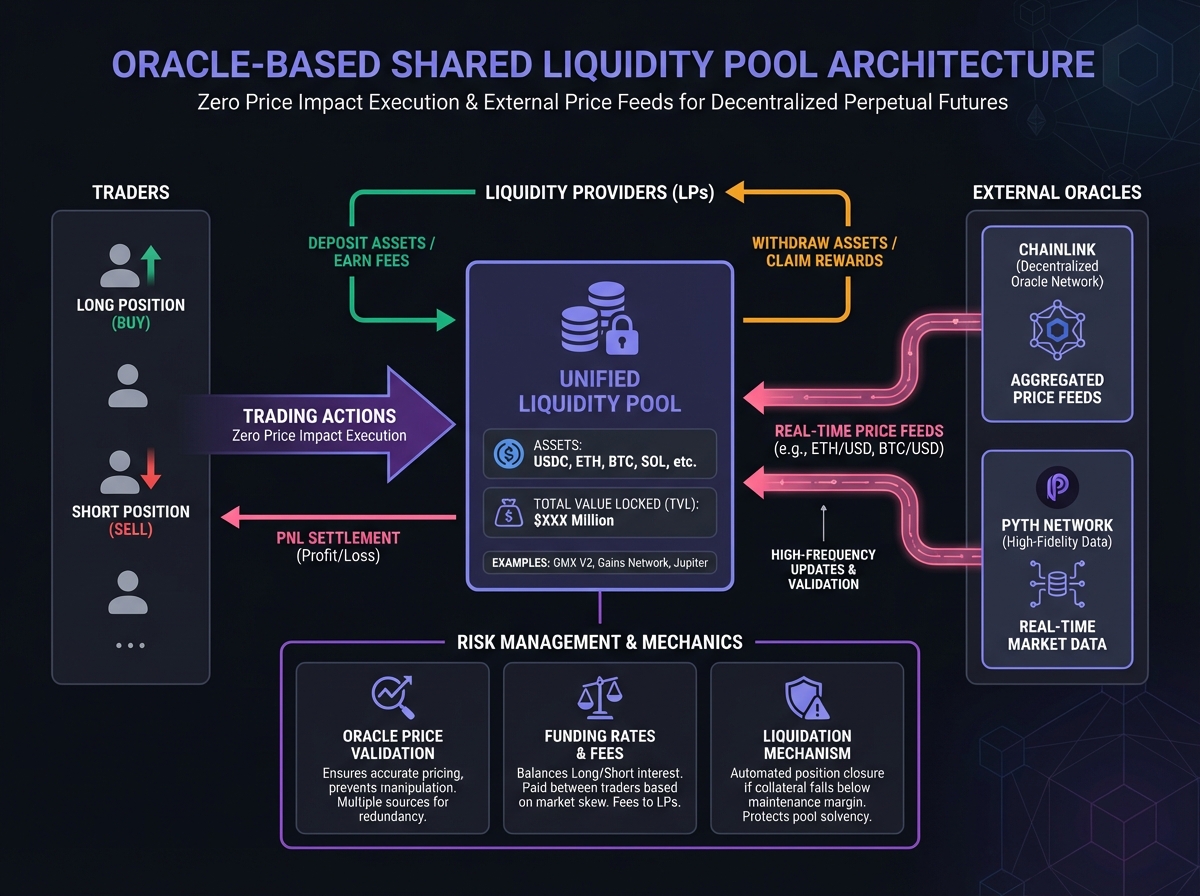

💧 Model 2: Oracle-Based Shared Liquidity Pools

How Oracle Pools Work

This model eliminates the order book entirely:

- Liquidity Providers (LPs) deposit assets into a unified pool

- Traders trade against the pool (not other traders)

- Prices come from external oracles (Chainlink, Pyth)

- Zero Price Impact (executed at oracle price)

Think of it like: Trading against a casino—the house (pool) is always the counterparty.

Oracle Pool Mechanism

Examples: GMX V2, Gains Network, Jupiter

How It Works:

- LPs deposit assets (ETH, BTC, USDC) into pool

- Pool acts as counterparty to all trades

- Oracle provides price (from Binance, Coinbase, etc.)

- Trades execute at oracle price (zero slippage)

- If trader wins → pool pays; if trader loses → pool collects

Key Innovation: No need for market makers or order books. The pool provides infinite liquidity (up to pool size) at the oracle price.

Oracle Pool Characteristics

| Feature | Description |

|---|---|

| Price Discovery | External (oracle feed from CEXs) |

| Slippage | No (zero price impact at oracle price) |

| Liquidity Source | LPs depositing into pool |

| Latency Risk | Oracle latency arbitrage |

| Trader Experience | Swap-like, simple execution |

| Capital Efficiency | Very high for LPs (one pool for all trades) |

Benefits of Oracle Pools

- ✅ Zero Slippage: Execute any size at oracle price

- ✅ Simple UX: No need to understand order books

- ✅ Deep Liquidity: Pool aggregates all LP capital

- ✅ No Market Makers Needed: Pool provides liquidity

Risks of Oracle Pools

- ❌ Oracle Latency: Price updates lag real market

- ❌ Toxic Flow: Arbitrageurs exploit stale prices

- ❌ Pool Insolvency: If traders win big, pool can drain

- ❌ No Price Discovery: Prices come from external sources

🔄 Model 3: Virtual AMM (vAMM)

How vAMM Works

The vAMM model adapts the constant product formula for synthetic leverage:

- No Real Assets: Virtual tokens in the curve

- Price Discovery: Algorithmic (based on virtual reserves)

- Real Collateral: Stored in smart contract vault

- Arbitrage Required: To keep price aligned with spot

Examples: Perpetual Protocol (original), modern iterations with oracle safeguards

How It Works:

- Virtual pool uses formula: $x \cdot y = k$

- No real assets swapped—just virtual reserves

- Real collateral stored in vault

- Price calculated from virtual token ratio

- Arbitrageurs keep vAMM price aligned with spot

vAMM Characteristics

| Feature | Description |

|---|---|

| Price Discovery | Internal (algorithmic curve) |

| Slippage | Yes (depends on k-value) |

| Liquidity Source | LPs providing virtual tokens |

| Latency Risk | Front-running transactions |

| Trader Experience | Swap-like |

| Capital Efficiency | Moderate (requires arbitrage) |

Benefits of vAMM

- ✅ Fully On-Chain: No external oracles (initially)

- ✅ Decentralized: Price discovery on-chain

- ✅ Simple Model: Easy to understand

Risks of vAMM

- ❌ High Slippage: Large trades move price significantly

- ❌ Arbitrage Dependency: Needs active arbitrageurs

- ❌ Price Divergence: Can drift from spot if arbitrage insufficient

- ❌ Modern Iterations: Often add oracle safeguards (hybrid model)

📊 Comparative Analysis Table

| Feature | CLOB | Oracle Pools | vAMM |

|---|---|---|---|

| Examples | dYdX, Hyperliquid, Vertex | GMX, Gains, Jupiter | Perpetual Protocol |

| Price Discovery | Internal (Supply/Demand) | External (Oracle Feed) | Internal (Algorithmic) |

| Slippage | Yes (depends on depth) | No (Zero slippage) | Yes (depends on k-value) |

| Liquidity Source | Market Makers | LPs (Public Pool) | LPs (Virtual Tokens) |

| Latency Risk | Front-running orders | Oracle latency arbitrage | Front-running transactions |

| Trader Experience | CEX-like, limit orders | Swap-like, simple | Swap-like |

| Capital Efficiency | High (market makers) | Very High (pooled) | Moderate (arbitrage needed) |

| Complexity | Medium (understand order book) | Low (simple execution) | Medium (understand curve) |

🎓 Beginner's Corner: Which Architecture Should You Choose?

Choose CLOB If:

- You want CEX-like experience (limit orders, stop losses)

- You're comfortable with order books

- You need precise entry/exit prices

- You're an active trader (scalping, day trading)

Best For: Professional traders, market makers, active day traders

Choose Oracle Pools If:

- You want simple execution (swap-like)

- You need zero slippage on large orders

- You don't want to worry about order book depth

- You prefer passive liquidity provision

Best For: Casual traders, large position traders, LP providers

Choose vAMM If:

- You want fully on-chain price discovery

- You're comfortable with AMM mechanics

- You understand arbitrage dynamics

- You prefer decentralized models

Best For: DeFi natives, arbitrageurs, protocol enthusiasts

🔬 Advanced Deep-Dive: Hybrid Architectures

Many modern protocols combine elements of multiple models:

Drift Protocol: The Liquidity Trifecta

Drift uses a three-layer system:

- JIT Auction: Market makers compete to fill orders

- DLOB: Decentralized limit order book

- DAMM: Dynamic AMM as backstop

This hybrid approach:

- Protects LPs from toxic flow (JIT makers step in first)

- Provides order book precision (DLOB)

- Ensures liquidity always exists (DAMM backstop)

GMX V2: Isolated Pools

GMX V2 moved from unified pool (GLP) to isolated pools:

- Each market has its own pool (ETH pool, BTC pool, etc.)

- Risk isolation (one market failure doesn't affect others)

- Still oracle-based (zero slippage)

- More capital efficient for LPs (choose exposure)

Extended: Unified Margin + CLOB

Extended combines:

- CLOB for order book trading

- Unified Margin across all positions

- Yield-Bearing Collateral (stETH, sDAI)

- Account Abstraction for EVM compatibility

This creates a "super-app" experience with advanced features.

⚠️ Critical Risk Differences by Architecture

CLOB Risks

- Slippage Risk: Large orders move price

- Front-Running: MEV bots can front-run your orders

- Liquidity Risk: Thin order books = high slippage

- Market Maker Dependency: Need active makers for liquidity

Oracle Pool Risks

- Oracle Latency: Stale prices = arbitrage opportunities

- Toxic Flow: Informed traders exploit pool

- Pool Insolvency: If traders win big, pool can drain

- Oracle Manipulation: Rare but possible

vAMM Risks

- High Slippage: Large trades move price significantly

- Arbitrage Dependency: Needs active arbitrageurs

- Price Divergence: Can drift from spot

- Capital Inefficiency: Requires large k-value for depth

📈 Real-World Examples

Example 1: Large Order on CLOB

Scenario: Want to buy $100,000 worth of ETH perp on Hyperliquid

- Order Book Depth: $50,000 at best bid

- Result: Your order will move price (slippage)

- Solution: Split into smaller orders or use limit orders over time

Example 2: Large Order on Oracle Pool

Scenario: Want to buy $100,000 worth of ETH perp on GMX

- Oracle Price: $2,500

- Pool Depth: $50M

- Result: Execute at $2,500 (zero slippage)

- Solution: No solution needed—just execute

Example 3: Funding Rate Arbitrage

Scenario: ETH perp funding rate is 0.1% per hour (very high)

- CLOB: Can't easily arbitrage (slippage costs)

- Oracle Pool: Can arbitrage (zero slippage)

- Result: Oracle pools better for arbitrage strategies

🔑 Key Takeaways

- Architecture determines risk profile: CLOB = slippage risk, Oracle = oracle risk

- CLOB offers CEX-like experience: Limit orders, stop losses, order book depth

- Oracle pools offer zero slippage: But face oracle latency and toxic flow risks

- vAMM offers on-chain price discovery: But requires arbitrage and has slippage

- Hybrid models combine benefits: Modern protocols use multiple layers

- Choose based on strategy: Active trading = CLOB, Large orders = Oracle pools

🚀 Next Steps

- Proceed to Lesson 4 to learn how to open your first position

- Explore different protocols to see architectures in action

- Consider which architecture fits your trading style

- Complete Exercise 3 to practice architecture analysis

Next Lesson: In Lesson 4, we'll explore opening your first perpetual position.