Lesson 9: Funding Rate Arbitrage Strategies

🎯 Core Concept: Capturing Funding Rates Without Price Risk

Funding rate arbitrage is a sophisticated strategy that allows you to earn funding payments while eliminating price exposure. By combining spot positions with perpetual positions, you can create delta-neutral portfolios that profit from funding rate differentials.

Why Funding Arbitrage Matters

Funding rates can be extremely profitable:

- High rates: 0.1% per hour = 876% APR

- Delta-neutral: No price risk (if executed correctly)

- Passive income: Earn while you sleep

- Scalable: Works with large capital

The Opportunity: When funding rates are high, you can capture them without betting on price direction.

💰 Strategy 1: Delta-Neutral Yield Farming

The Basic Setup

Concept: Long spot + Short perpetual = Delta neutral

How It Works:

- Buy spot asset (e.g., 1 ETH at $2,500)

- Open short perpetual (1 ETH notional, 1x leverage)

- Net exposure: ~0 (delta neutral)

- Earn funding rate (if positive, shorts receive)

Example:

- Buy 1 ETH spot: $2,500

- Short 1 ETH perp: $2,500 notional

- Funding rate: 0.05% per hour (positive)

- Daily funding received: $2,500 × 0.0005 × 24 = $30

- Annualized: 438% APR

Key Insight: You earn funding regardless of price movement (if delta neutral).

Execution Steps

Step 1: Identify Opportunity

- Find market with high positive funding rate

- Check annualized rate (>50% is attractive)

- Verify liquidity on both spot and perp

Step 2: Calculate Position Sizes

- Spot position: $X

- Perp position: $X (1x leverage, same notional)

- Ensure delta neutrality

Step 3: Execute Simultaneously

- Buy spot first (or use limit orders)

- Open short perp immediately

- Monitor delta (should be ~0)

Step 4: Monitor and Adjust

- Check funding rate changes

- Rebalance if delta drifts

- Close when funding becomes unfavorable

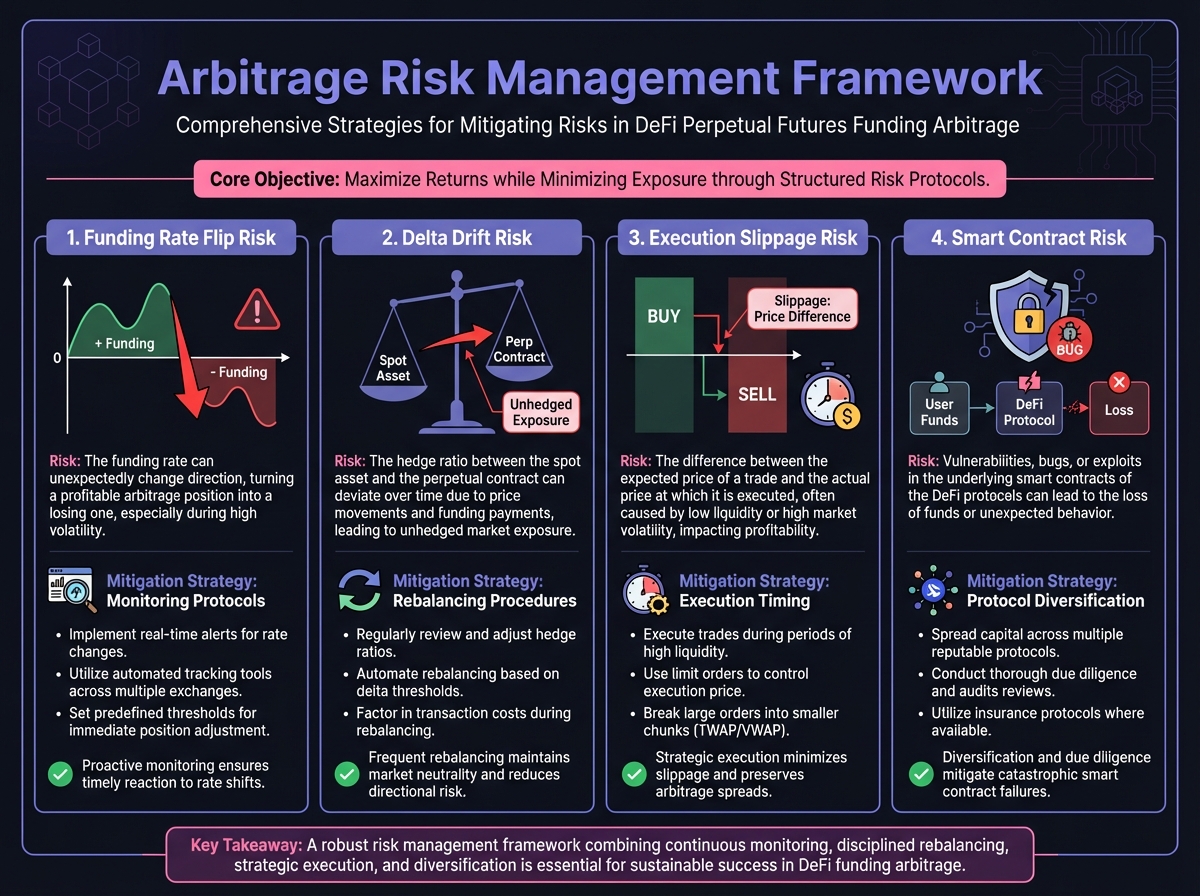

Risks and Mitigation

Risk 1: Funding Rate Flips

- Problem: Positive funding becomes negative

- Impact: You now pay instead of receive

- Mitigation: Monitor rates, close if flips

Risk 2: Delta Drift

- Problem: Positions become unbalanced

- Impact: Price exposure re-emerges

- Mitigation: Regular rebalancing

Risk 3: Execution Slippage

- Problem: Can't execute simultaneously

- Impact: Temporary price exposure

- Mitigation: Use limit orders, execute during low volatility

Risk 4: Smart Contract Risk

- Problem: Protocol exploits or failures

- Impact: Loss of capital

- Mitigation: Diversify across protocols, use audited platforms

🔄 Strategy 2: Cash and Carry Basis Trade

The Concept

Basis: Difference between perpetual price and spot price

Cash and Carry: Exploit basis by shorting perp and buying spot

How It Works:

- If perp > spot: Short perp, buy spot

- Funding rate forces convergence

- Capture the basis spread

Example

Setup:

- Spot ETH: $2,500

- Perp ETH: $2,600

- Basis: $100 (4%)

- Funding rate: 0.1% per hour (very high)

Execution:

- Buy 1 ETH spot: $2,500

- Short 1 ETH perp: $2,600

- Initial profit: $100 (basis capture)

- Ongoing: Earn funding rate

Convergence:

- Funding rate forces perp price toward spot

- When they converge, close both positions

- Total profit: Basis + Funding received

When to Use

Ideal Conditions:

- Large basis (>2%)

- High funding rate

- Expected convergence

- Sufficient liquidity

Avoid When:

- Basis is small (<0.5%)

- Funding rate is low

- High execution costs

- Illiquid markets

🌐 Strategy 3: Cross-Protocol Arbitrage

The Opportunity

Different protocols, different funding rates:

- Protocol A: 0.05% per hour

- Protocol B: 0.02% per hour

- Difference: 0.03% per hour arbitrage

Execution

Setup:

- Long on Protocol A (paying 0.02%)

- Short on Protocol B (receiving 0.05%)

- Net: Receive 0.03% per hour

Example:

- Position size: $10,000 each side

- Funding received (Protocol B): $12/day

- Funding paid (Protocol A): $4.80/day

- Net profit: $7.20/day

- Annualized: 26.3% APR

Considerations

Challenges:

- Bridge costs between protocols

- Different liquidation mechanics

- Monitoring complexity

- Capital requirements (need margin on both)

Benefits:

- Diversified risk (not single protocol)

- Capture rate differentials

- Scale across multiple venues

📊 Strategy 4: Funding Rate Prediction

The Concept

Predict funding rate changes before they happen

Indicators:

- Open Interest trends

- Price momentum

- Market sentiment

- Historical patterns

Execution

Setup:

- Monitor OI and price trends

- Predict funding will increase

- Position before rate spikes

- Capture high rates early

Example:

- Current funding: 0.01% per hour

- OI becoming imbalanced (80% Long)

- Predict funding will spike to 0.05%

- Open short position early

- Capture full 0.05% when it spikes

Risks

Prediction Risk:

- Funding may not spike as expected

- OI may rebalance quickly

- Market conditions change

Mitigation:

- Use multiple indicators

- Start with small positions

- Monitor closely

- Have exit strategy

🎓 Beginner's Corner: Simple Funding Capture

Your First Arbitrage

Start Small:

- Capital: $1,000

- Market: ETH (most liquid)

- Protocol: GMX V2 (zero slippage)

Steps:

- Check ETH funding rate on GMX

- If >0.02% per hour, proceed

- Buy $500 ETH spot (on Uniswap or CEX)

- Short $500 ETH perp on GMX (1x leverage)

- Monitor daily

- Close when funding flips negative

Expected Return:

- Funding: 0.02% per hour = 175% APR

- On $500 perp: ~$2.40/day

- After gas and fees: ~$2/day

- Monthly: ~$60 (6% on $1,000)

Key: Start small, learn mechanics, scale gradually.

🔬 Advanced Deep-Dive: Optimized Arbitrage

Multi-Asset Strategies

Diversification:

- ETH arbitrage: $5,000

- BTC arbitrage: $5,000

- SOL arbitrage: $5,000

- Total: $15,000 capital

Benefits:

- Diversified across assets

- Capture best rates across markets

- Reduce single-asset risk

Automated Strategies

Bot Requirements:

- Monitor funding rates across protocols

- Execute when opportunities arise

- Rebalance automatically

- Risk management rules

Considerations:

- Development costs

- Monitoring infrastructure

- Gas optimization

- Risk of bugs

Yield-Bearing Collateral Enhancement

Extended/Drift Advantage:

- Use stETH as collateral

- Earn staking yield (4% APR)

- Plus funding arbitrage (10% APR)

- Total: 14% APR delta-neutral

Example:

- Deposit $10,000 stETH

- Open short ETH perp

- Earn: Staking yield + Funding

- Net cost: Minimal (funding may offset)

⚠️ Critical Risks

Funding Rate Volatility

The Problem: Rates can flip quickly

Example:

- Open short at 0.05% per hour (receiving)

- Market sentiment shifts

- Rate flips to -0.05% per hour (paying)

- Now losing money

Mitigation: Set alerts, monitor closely, have exit plan

Execution Risk

The Problem: Can't execute simultaneously

Example:

- Buy spot ETH at $2,500

- Try to short perp, but price moved to $2,520

- Now have $20 price exposure

Mitigation: Use limit orders, execute during low volatility, accept small exposure

Protocol Risk

The Problem: Smart contract exploits

Example:

- Protocol gets hacked

- Funds locked or stolen

- Arbitrage position can't be closed

Mitigation: Diversify, use audited protocols, monitor security

Capital Efficiency

The Problem: Need capital for both sides

Example:

- Want $10,000 arbitrage

- Need $10,000 for spot

- Need $10,000 margin for perp

- Total: $20,000 required

Mitigation: Use protocols with cross-margin, leverage spot (carefully)

📊 Real-World Example: Complete Arbitrage Setup

Opportunity:

- ETH spot: $2,500

- ETH perp: $2,550 (basis: 2%)

- Funding rate: 0.03% per hour (positive)

- Annualized: 262% APR

Execution:

- Buy 4 ETH spot: $10,000

- Short 4 ETH perp: $10,000 notional

- Initial profit: $200 (basis capture)

- Daily funding: $7.20/day

- Monthly: $216 + $200 = $416

ROI: 4.16% monthly on $10,000 capital

Monitoring:

- Check funding rate daily

- Rebalance if delta drifts >5%

- Close if funding flips negative

- Target: Hold until basis converges

🛠️ Arbitrage Tools

Use these calculators to plan your arbitrage strategies:

Funding Rate Calculator

Launch Funding Rate Calculator →

Delta-Neutral Position Builder

Launch Delta Neutral Builder →

🔑 Key Takeaways

- Delta-neutral yield farming captures funding without price risk

- Cash and carry exploits basis between spot and perp

- Cross-protocol arbitrage captures rate differentials

- Funding prediction can enhance returns

- Start small, learn mechanics, scale gradually

- Monitor closely—rates can flip quickly

- Diversify across assets and protocols

- Use yield-bearing collateral when possible

🚀 Next Steps

- Proceed to Lesson 10 to learn advanced risk management

- Complete Exercise 9 to design your arbitrage strategy

- Start with small positions to learn

- Monitor funding rates across protocols

Next Lesson: In Lesson 10, we'll explore risk management and position protection.